This article is adapted from Nepal Economic Forum's 25th issue of Nefport.

Although a bit late, the government is finally gearing up to formulate a long-term vision for economic development. The tentative targets for now are to graduate from the Least Developed Country (LDC) status by 2022 and to attain the slew of Sustainable Development Goals by 2030. However, a bold and time-bound economic development vision for the country should go beyond these goalposts that were contextualized on the basis of global targets. Nepal should aim to become a vibrant lower-middle income economy within the next two decades.

At the core, it essentially means increasing gross national income (GNI) per capita (World Bank’s Atlas method) from existing USD 730 to about USD 4,125 (the threshold between lower-middle income and upper-middle income economy). In order to achieve such a goal, it is essential that the government draw up a list of strategic flagship projects in physical and social infrastructure sectors and execute them with an efficient and workable implementation arrangement that is in sharp departure from the current discouraging project implementation ecosystem.

Given an appropriate mix of macroeconomic strategy, financial arrangement, smart project execution and supportive institutions, a meaningful structural transformation is possible and the stated goals are achievable. This piece focuses on the macroeconomic aspect of marching on that path.

Macroeconomic essentials

A large amount of public and private investment is required to increase income per capita by almost six folds within two decades. The scale and scope of public investment would depend on revenue mobilization, rationalization of ballooning recurrent spending, and foreign aid. Meanwhile, private investment would depend on investor-friendly environment, including protection of investment and returns, supportive laws and policies, mechanisms for sharing of risk, returns and technology (such as public private partnerships), and maturity of the financial market, among others.

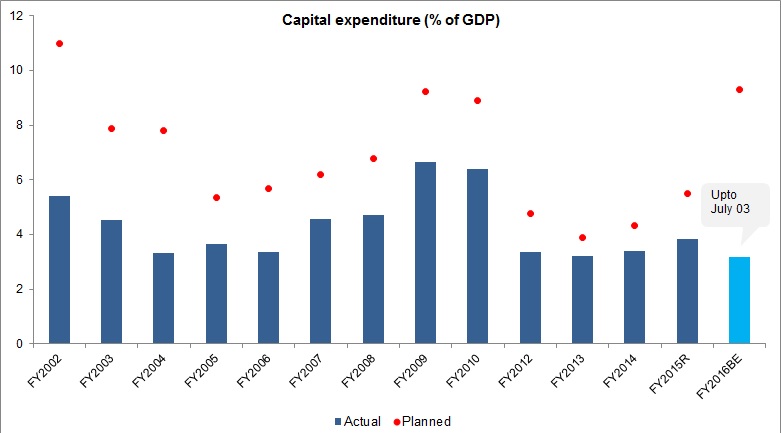

Overall, sound macroeconomic environment will be at the heart of financing for such large scale public and private investment. At around 21% of GDP, the gross fixed investment is lower than the average for low income countries. This needs to be over 30% of GDP to accelerate growth rate (beyond the contribution by exogenous factors such as monsoon and remittances), which will then boost income per capita, and employment generation, primarily through investment in productivity-enhancing physical and social infrastructure. Specifically, public fixed capital investment has to increase to about 10% of GDP over the next decade from the existing 4.5% of GDP.

On the financing part, a combination of rationalization of recurrent expenditure, higher domestic revenue, domestic borrowing, and higher grants as well as concessional and non-concessional loans are needed. At the current level and growth of recurrent expenditure, it will be challenging to cover it sustainably by tax revenue, whose growth rate has stagnated at around 15%. Hence, trimming wasteful recurrent spending in uncoordinated programs and projects should be a priority as a part of sound fiscal management to attain the long-term vision. Second, along with efforts to expand the tax base, the revenue administration will have to be made more efficient and responsive. The present revenue system is too dependent on taxes on remittance-financed imported goods and services. Third, domestic borrowing has to be managed judiciously keeping in mind the optimum market liquidity. Finally, foreign assistance needs to be better utilized by enhancing expenditure absorption capacity. These will partly cover the required resources for public sector investment.

Additionally, fiscal and monetary policies need to be synchronized to tame inflation so that it is not persistently and prohibitively high to discourage investment. At present, inflation is mostly a supply-side phenomenon although localized sectoral inflation (such as unnatural escalation of real estate and housing prices few years back) is mostly within the ambit of monetary authorities. More generally, monetary policy can support the vision by creating appropriate incentives to channel savings into infrastructure investment that typically pay-off in the long-term. Finally, external sector stability should not be much of an issue as long as the economy is gradually diversified and production is competitive in addition to a net positive transfers and sizable foreign exchange reserves.

Supportive environment

An investment-friendly environment is essential to increase domestic as well as foreign investment. While a slew of laws need updating, policies need rewriting to facilitate and simplify investment rules and approvals. In the meantime, drastic enhancement of capital spending absorption capacity is required to increase public spending in infrastructure, a lack of which is the most binding constraint to inclusive economic growth. Supportive institutions that can foster creative creation and creative destruction need to be promoted as opposed to the protection of business interests through syndicates and cartels. This is crucial for entrepreneurial spirit and to incentivize saving, investment and innovation. Inclusive political and economic institutions are vital to sustaining an equitable and rising income per capita. It is also important to change the course of out-migration for jobs and improved opportunities, and to enhance external sector competitiveness.

Structural transformation

A meaningful structural transformation underpins the pace and pattern of economic growth. Along with the decline of the agricultural sector, Nepal is seeing the rise of low value added, low productivity services sector activities. This structural shift is bypassing industrial sector growth (a sort of deindustrialization), which is vital for productive employment, sustained rise in income per capita, and high growth rate initially. Reversing this trend and revitalization of industrial sector along with promotion of high value added agriculture and services sector activities, with an employment centric strategy to absorb the surplus labor, should form the core of the structural transformation process, which will then lead to higher and inclusive economic growth.

With the right mix of reforms and policies, supportive institutions, enhancement of absorption capacity, and a sound macroeconomic environment to support such structural transformation, the likelihood of attaining the long-term vision is high.